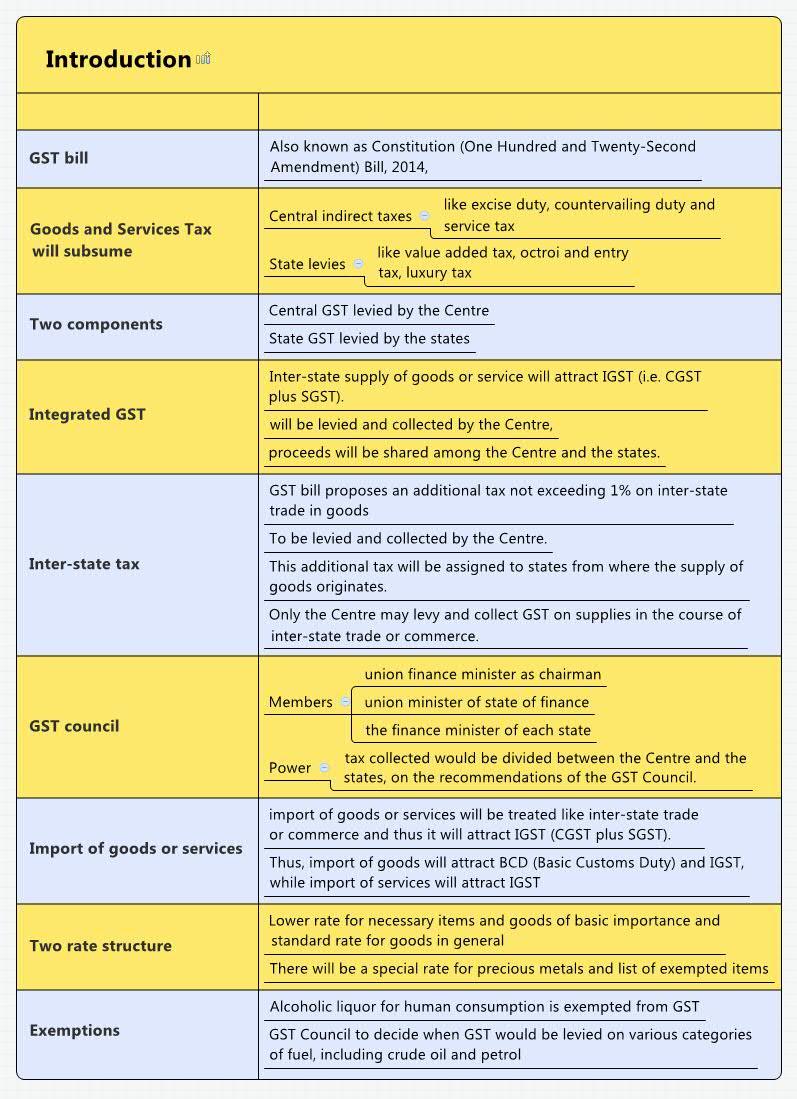

GST bill

GST bill

Introduction

Development of GST (Pre-VAT to model GST)

Pre-VAT

- Prior to VAT, excise duty was levied on both inputs used and the output produced. This was applicable to each intermediate good in the manufacturing process.

- This “tax on tax‟ led to cascading of taxes.

VAT

- The concept of Value Added Tax (VAT) was introduced for central excise duty in 1986 (first as MODVAT and then as CENVAT).

- The issue of cascading taxation was partly addressed through the VAT regime.

- However, certain problems remained. For example, several central and state taxes were excluded from VAT.

- Sectors such as real estate, oil and gas production etc. were exempt from VAT.

- Further, goods and services were taxed differently, thereby making the taxation of products complex.

Post VAT

- Some of these challenges are sought to be overcome with the introduction of the Goods and Services Tax (GST).

- GST regime intends to subsume most indirect taxes under a single taxation regime.

- GST is expected to help:-

- Broaden the tax base

- Increase tax compliance

- Reduce economic distortions caused by inter-state variations in taxes

GST bill, 2014

(Explained on the top)

Draft model GST bill, 2016

Following are the salient features of draft GST bill:-

- All forms of “supply” of goods and services will attract CGST (central levy) and SGST (state levy).

- The liability to pay CGST or SGST will arise at the time of supply.

- Erstwhile taxable heads such as “manufacture”, “sale” and “provision of services”, among others, will lose relevance.

- States will draft their own State GST based on the draft model law with minor variations

- GST would be payable on “transaction value”, being the price actually paid or payable.

- As the threshold limit, the draft GST Bill proposes Rs 10 lakh, and for Northeast states and Sikkim, an amount of Rs 5 lakh.

Benefits

- GST will reduce the complexity of taxes.

- It can facilitate seamless movement of goods across states.

- It will reduce the transaction costs of businesses.

- The procedure of GST registration would also be made simple, thereby improving the ease of starting a business in India.

- There are expectations among experts that with GST, we may see 2% jump in GDP growth.

- GST will plug the leakage of tax. This, in turn, gives more money in the government exchequer.

- Companies which are under unorganized sector will come under the tax regime.

- Number of tax departments will reduce which in turn may lead to less corruption.

- In the long run, the lower tax burden can decrease the prices of goods and services.

Challenges

- The main road block is the coordination among states and center and states.

- Another major hurdle is getting the constitution amended by agreement of both the houses.

- Consensus on uniform GST rates

- Inter-state transaction of goods and services

- Administrative efficiency

- Infrastructural preparedness to implement the new tax reform

Criticisms

- Some has argued that, whatever federal powers were bestowed upon States by virtue of their powers to tax, will be lost once the GST Bill becomes law.

- As per the current arrangements, dispute settlement would be subjected to lengthy court procedures, if the Council is opposed, as GST Dispute Settlement Authority in the proposed Bill will only comply with the jurisdiction of the Supreme Court.

- India is adopting a dual GST, wherein the Central GST will be called CGST and state SGST.

- Some critics consider GST to be a regressive tax, meaning the poor pay more, as a percentage of their income, than the rich.

- Opposition wants a provision capping the GST rate at 18 per cent to be added to the Bill itself.

- Deferring the levy of GST on five petroleum products could lead to cascading of taxes.

- Additional 1% tax levied on goods that are transported across states dilutes the objective of creating a harmonized national market for goods and services.

- Inter-state trade of a good would be more expensive than intra-state trade, with the burden being borne by retail consumers.

Leave a Reply